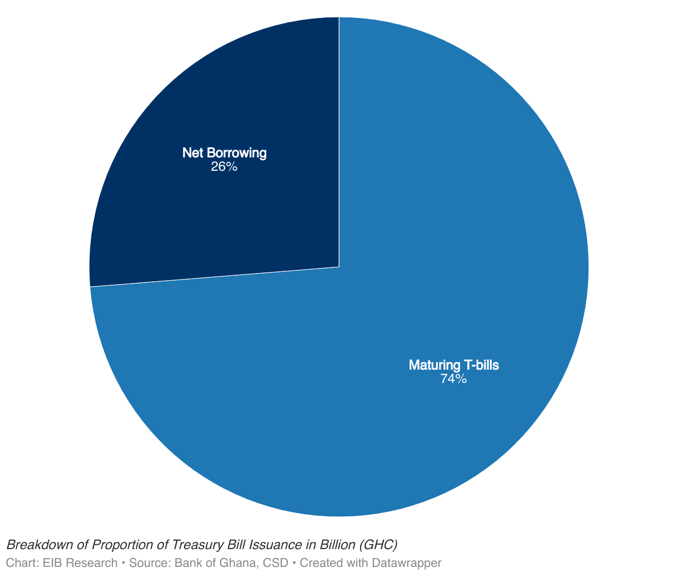

An analysis of government borrowing from the domestic market by the EIB Network has revealed that GHC 44.1 billion (nearly 75%) of the GHC 59.8 billion borrowed by the new government over the last seven weeks on the treasury market was used to service matured treasury bills issued in 2024.

The issue of government borrowings came to the fore once again when Dr. Gideon Boako, the Tano North MP and Economic Advisor to Former Vice President Dr. Mahamudu Bawumia, accused the Mahama-led government of borrowing in excess of GHC 20 billion within its first month in office.Dr. Boako will further advance his claims accusing the government of reneging on its promise to reduce borrowing and drive rates down during the vetting of deputy finance minister designate, Thomas Ampem Nyarko.

“If you follow the trend within January alone, contrary to what we have been told by the government that we want to cut the borrowing and bring the rates down, this government in four weeks has borrowed Cedis 38.5 billion”, Dr. Boako put to the nominee.

But despite Mr. Apem Nyarko’s challenge of the accuracy of the claims and subsequent assertions that briefings he received indicated that the new government had borrowed on net basis far lower than what put out, the minority in parliament including former deputy finance minister, Dr. Stephen Amoah have insisted the government has borrowed over GHC 50 billion in its first 50 days in office.

An analysis of treasury issuance data has confirmed that the actual fresh borrowing (net borrowing) by the government is GHC 15.7 billion. This is because GHC 44.1 billion was used to either roll over or pay matured treasury bills issued.

Breakdown attached below:

This GHC 44.1bn catered for matured bills as follows:

364-day bills issued between January and February 2024

182-day bills issued between July and August 2024

91-day bills issued between November and December 2024 This effectively means, that for every GHC 4 that the government raised in treasury bills, GHC 3 was used to roll over old debt and GHC 1 as new debt to finance government operations.

Further analysis of the GHC 15.7 billion in fresh borrowing reveals that this amount was anticipated in the mini-budget presented and approved by the 8th Parliament on January 3, 2025, before its expiration.

Due to Ghana’s exclusion from the international bond market over the last two years and the existing memorandum of understanding (MoU) under the IMF program, which prohibits central bank financing of government deficits, the government has had to rely heavily on domestic revenue—particularly treasury bills—to address budget shortfalls. (Government in the first quarter of 2024 had planned to raise close to GHC 20 bn in fresh securities to finance its activities).

In the first quarter of 2024, the government had planned to raise close to GHC 20 billion in fresh securities to finance its activities. Similarly, the 2025 Expenditure in Advance of Appropriation projected a budget deficit of GHC 24.3 billion for the first quarter of 2025, of which GHC 20.2 billion was expected to come from the domestic market. Based on this, it can be inferred that GHC 15.7 billion in fresh financing is still within the approved borrowing mark, and the government may require an additional GHC 5 billion to GHC 9 billion in the upcoming months to fulfill the country’s expenditure needs.

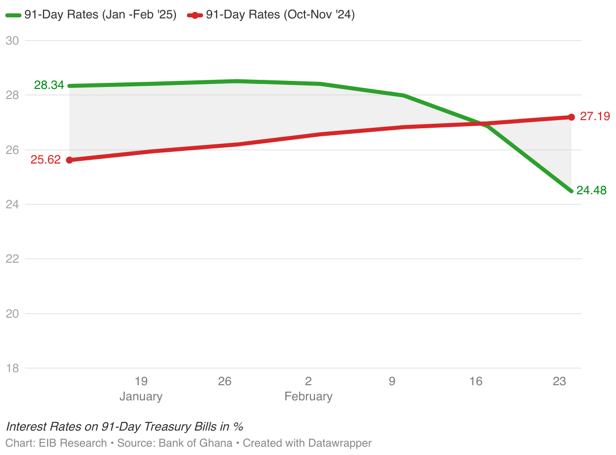

On the cost of borrowing on the treasury market, the government, under its new debt management strategy, has rejected billions in bids deemed overpriced, leading to a decline in interest rates across all three treasury bill maturities. 91-day and 182-day bills auctioned on February 21 sold at lower rates than similar bills issued 91 and 182 days prior.

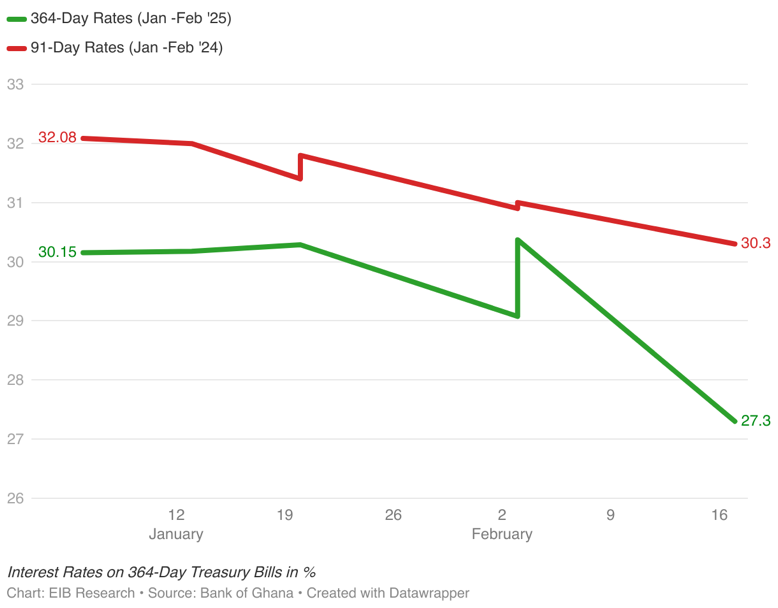

The 364-day bills on the other hand had all 6 tranches issued thus far, selling cheaper than they sold a year prior, experiencing a rapid fall from 30.15% to 27%.

With treasury bills remaining the government’s safest option for financing short-term needs, it remains to be seen whether the downward trend in borrowing costs can be sustained.